Exchanging Planes for Pelotons: Investigating Covid-19’s Impact on Consumer Spending

- Harvard Economics Review

- Jul 27, 2020

- 5 min read

By: Julia Manso

As Covid-19 morphed from localized epidemic to a global pandemic in March of 2020, economic policymakers across the globe could sense the impending financial crisis that would accompany the virus’ threat to human health. The writing was on the wall—but what exactly did it say?

Most national and international economic organizations recognized that a sharp decline in consumer spending, catalyzed by a decrease in consumer demand and rise in unemployment, was at the core of a massive economic contraction. Accompanying this demand-side contraction were serious supply shocks and a collapse of commodity prices early in the pandemic. Governments realized a timely and immediate response was necessary, but struggled to effectively balance—or even minimize—the decline in consumer spending with these supply-side issues and falling commodity prices. In one of the first waves of response, the United States’ Federal Reserve Bank reduced interest rates to stimulate economic activity while providing liquidity to financial markets. But regardless of the government’s measures, the pandemic was sure to wreak havoc on consumer spending.

Early analysis from the U.S.’s Bureau of Economic Analysis (BEA) stated that Americans were dramatically cutting back expenditures in the wake of Covid-19 with the decline in consumer expenditure contributing -5.3 percentage points to the first quarter’s contraction and helping to drive the real GDP contraction of 4.8 percent annualized for the first quarter of 2020.

Similarly, amid strict lockdown rules that led to closed storefronts and limited travel, the World Economic Forum (WEF) predicted in May of 2020 that the United States would have a unilateral pullback in nearly all spending categories, except groceries, household supplies, and home entertainment. It likewise estimated an over 50 percent decrease in travel and transportation, apparel, services (pet care, fitness and wellness, personal care), and restaurants.

To facilitate a more in-depth understanding of how Covid-19 has impacted consumer spending, researchers Raj Chetty, Nathaniel Hendren, Michael Stepner, John Friedman, and the Opportunity Insights Team leveraged anonymized data from several private companies to construct indices of consumer spending, unemployment, and other variables. They ultimately built a new, freely-accessible platform, The Opportunity Insights Economic Tracker. Overcoming the traditional challenges of national data collection, such as low frequency collections, significant time lags, and statistics being available only for state or national levels, the platform provides high-frequency and granular level data on consumer spending levels across the U.S.

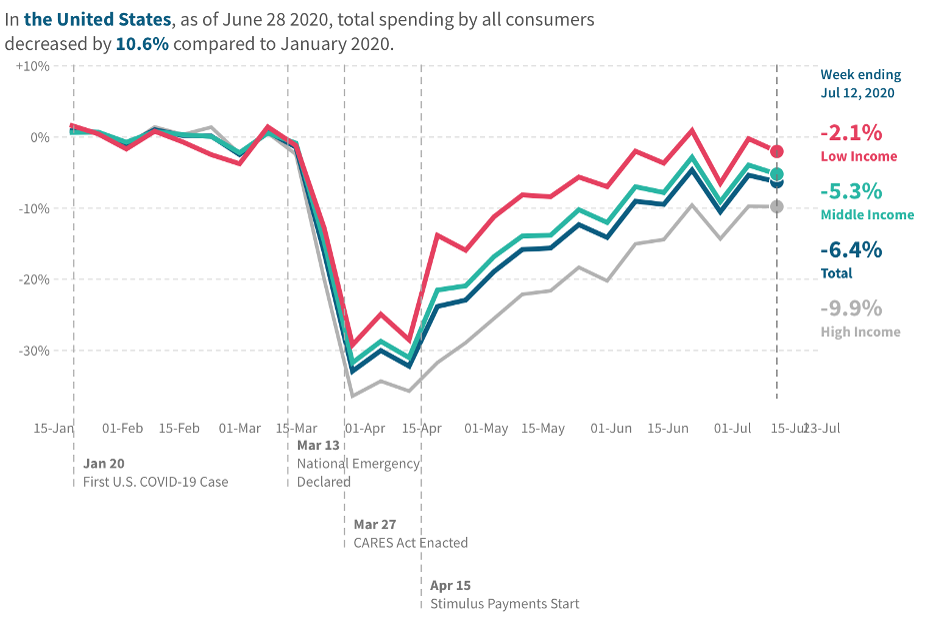

In their June 2020 working paper titled “How Did COVID-19 and Stabilization Policies Affect Spending and Employment? A New Real-Time Economic Tracker Based on Private Sector Data,” Chetty et al. highlight some of the key takeaways from the data, particularly emphasizing that most of the reduction in consumer spending in the U.S. came from reduced spending by high-income households, as illustrated in the chart below.

Source: www.tracktherecovery.org

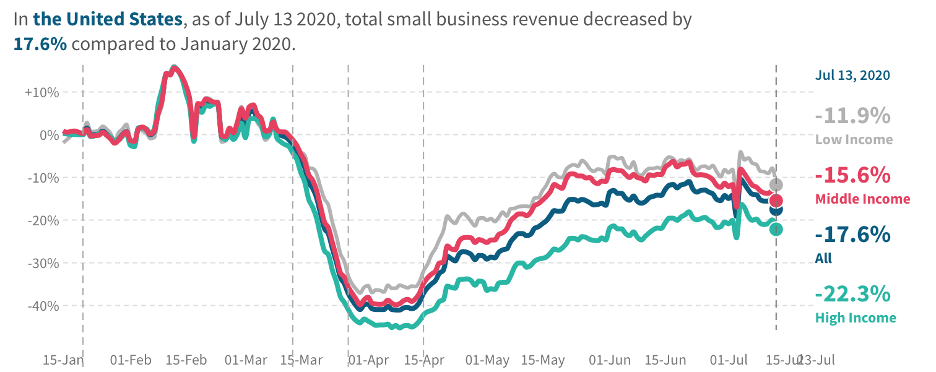

As a result, Chetty et al. found that small businesses in these high-income neighborhoods were most at risk of revenue loss and closure. As evidenced in the below chart illustrating small business revenue, revenue for businesses in high-income zip codes has fallen below that of businesses in low and middle income zip codes with the Covid-19 pandemic. While these businesses are closely clustered from January to early March, the arrival of Covid-19 and the drop in high-income spenders has adversely impacted businesses in high-income zip codes more so than those in middle to low income zip codes.

Source: www.tracktherecovery.org

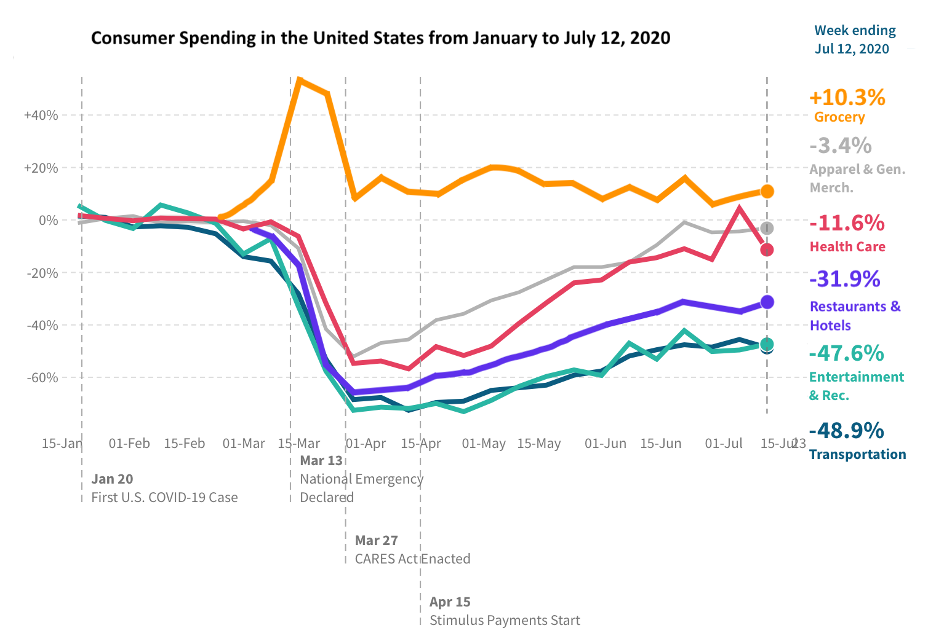

Going into the data, I ranked the hardest hit sectors nationally, as the latest data (from the week ending July 12, 2020) illustrates. The worst hit sector was transportation, which is currently 48.9 percent below January 2020 levels. Transportation was the first category to have a sharp decrease in consumer spending in 2020, already dropping 14 percent by March 1. At its lowest point, consumer spending on transportation was 72.8 percent below the January 2020 level in mid-April. Since then, it has consistently but slowly increased, but is still far below normal.

Not far behind transportation, arts, entertainment, and recreation experienced a 47.6 percent decline compared to January 2020 levels. Consumer spending dropped precipitously in mid-March, staying at or below a 70 percent decline from January 2020 throughout all of April.

The next hardest hit sector is restaurants and hotels, which is currently 30.9 percent below January 2020 levels. Like both transportation and arts, entertainment, and recreation, it experienced a precipitous drop in late March, and it has been rising since then.

Faring better than transport, healthcare is only 11.6 percent below January 2020 levels. After dropping in late-March to roughly 50 percent of January 2020 levels, consumer spending on healthcare has risen, spiking in early June to then drop back to 11.6 percent below January 2020 levels during the week ending on July 12.

Currently, apparel and general merchandise are 3.4 percent below January 2020 levels. While dropping to roughly 50 percent of January 2020 levels in late March, consumer spending on apparel and general merchandise has increased steadily, reaching its present level.

Grocery spending is an important anomaly, currently 10.3 percent above January 2020 levels. While all of the above industries experienced a precipitous drop during March, grocery spending rose rapidly, peaking at 53.8 percent above January 2020 levels in the week of March 15. Since March 1, grocery spending has consistently remained roughly around 10 percent above January 2020 levels.

The above graph depicts consumer spending by sector in the United States between January and mid-July 2020, illustrating which sectors have been most and least impacted by the pandemic.

Source: www.tracktherecovery.org, modified and colorized by the author.

Ultimately, based on the extensive private sector data collected and compiled by Chetty, Hendren, Stepner, Friedman, and the Opportunity Insights Team, the actual impact of Covid-19 on consumer spending diverges from both BEA and WEF predictions; it is not so much that all Americans are “drastically” cutting back spending, as the BEA predicted, but specifically that high-income Americans are cutting back. Low-income consumer spending is just 2.1 percent below January 2020 levels while middle-income spending is 5.3 percent below January levels, compared to high-income spending at 9.9 percent below January 2020 levels.

As expected, the WEF’s predictions on grocery spending increasing were correct. As the WEF estimated, transportation, entertainment & recreation, and restaurants & hotels all experienced sustained drops at or below 50 percent of the January 2020 level, yet somewhat surprisingly, apparel and general merchandise was an important exception, making nearly a v-shaped recovery as it hovers just below 3.4 percent of the January 2020 level.

While the majority of the decline in consumer spending comes from high-income households, the above data suggests that low-income individuals have benefited most from stimulus and unemployment checks. As illustrated in the first graph, spending rose very sharply for those at the bottom of the income distribution starting on April 15, when the stimulus payments began, and ultimately rose nearly 20 percentage points within a week. Also drawing this conclusion, Chetty et. al highlight that stimulus checks increased spending, though not necessarily in the sectors that have been most impacted by Covid-19. Transportation and entertainment & recreation, for example, were the hardest hit sectors, yet they experienced very modest gains over the two months after the stimulus checks were distributed. Due to the fundamental health concerns driving the contraction in consumer spending—particularly for high-income individuals who have reduced their spending most—traditional macroeconomic tools, such as providing liquidity to businesses, have a more limited impact. The data instead suggests that social insurance programs are effective in mitigating the effects of the pandemic, helping to bolster consumer spending, and will likely be a key policy tool in the coming months.

Ultimately, as Chetty et. al hints, the only path to full economic recovery in the hardest hit sectors will be to address and tackle the virus itself. Restoring consumer confidence will be essential in reviving consumer spending at all levels, for only when consumers are comfortable enough to regularly visit restaurants, go to theatres, and travel will the worst-hit sectors begin to recover. And to reach this point, health experts and policymakers will have to work together—and do better.

Comments